Life Insurance - CRS

Common Reporting Standard (CRS) is a new worldwide information gathering and reporting requirement for financial institutions (including insurance companies) in participating countries, to help fight against tax evasion and protect the integrity of the global tax system.

Please refer to our FAQ to learn more about CRS. You may also upload the Tax Residency Self-Certification Form at our Forms Menu.

Insurance Basics

What is Life Insurance?

Life insurance is to protect a person’s life over uncertainty that may occur to them at any point of time. The policyholder pays their premium regularly for an agreed amount of coverage and if the specified event such as death or an accident resulting in death or disability, the amount of coverage will be paid. Insurance is the sharing of risks between a large numbers of people. The life insurance fund is a pool of money derived from the premiums paid by all the policyholders and will be paid to those policyholder that is less fortunate or to their next of kin.

Why do I need Life Insurance?

Protection: It gives full protection against risk of death or disability. It provides financial support to you and your family when unexpected events occurred.

Savings: If the policy is a participating plan, Life Insurance can help you to save and plan for your future such as children education, invest for a better future, protect your loved ones and retirement income.

Am I having the right policy?

There are a few category of policy namely education, protection, wealth accumulation, medical insurance and retirement. There is “no right” policy purchased as it depends on your needs. Each stages of life will have different needs and therefore, different stage of life will focus on different category of policy. It is important to

a) Know your needs

Different people will have different needs and the reasons for purchasing policy can be due to the followings:

a) Continuity in income in the event of Death or Disability

b) Income for policyholder should he/she becomes critically ill

c) Savings or investments

d) Education for children

e) Plan for retirement income

f) Invest for a better future

b) Affordability

Individual will purchase insurance according to their needs and at the same time based on the affordability in paying such premium. Generally, Life insurance should be purchased according to one’s financial needs

What types of life insurance policies are available?

Life insurance policies can be categorized into With Profit (Participating) and Without Profit (Non-participating). Those policies With profits will share in the profits made by the life insurer where as those Non-participating plan does not. Therefore the Non- participating plan is relatively cheaper as compared to With Profit plan

The main types of life insurance plans are:

a) Whole Life provides for the payment of the sum assured only on the death of the life assured. Under this plan, premiums may be payable throughout life or for a limited period or up to an agreed age only. As the income of a person after retirement would normally be less than when he is in full working capacity, it is therefore desirable to take out a whole life assurance with a “limited payments” period. This type of policy is most suitable for the assured whose main concern is to make the best possible provision for his family in the event of his death because large amount of protection can be provided at a relatively small cost. The premium is relatively cheaper as compared to endowment plan.

b) Endowment provides saving and protection at the same time for the term of the policy. This type of policy can be bought for varying terms from 10 years and above, or up to a certain age. A guaranteed sum of money, the sum assured together with any bonuses attached (if any) will be payable upon the death of the life assured within the term of the policy. Should the policyholder survived throughout the term of the policy, he/she will received the sum assured together with the attached bonuses (if any). Premiums are paid throughout the policy term.

There is another plan with limited payment term where the policyholder may choose a premium payment term that he/she can best afford. The shorter the premium payment terms, the higher will be the discount.

There is a endowment plan where the partial maturity payment will be paid in instalment throughout the term. This type of endowment policy is called Anticipated Endowment Plan.

c) Term - This is an assurance for a specified period and the sum assured is payable only on the death of the life assured during that period. If he survives that term he gets nothing although he will have paid all his premiums regularly. This type of assurance provides the maximum immediate cover at the lowest cost and is usually effected by the creditor on the life of the debtor.

d) Supplementary Benefits or Riders - This is an additional benefits that are not included in the main plans. These include benefits for accidental assurance, hospitalization, medical expenses, death or disablement due to accidents and income protection, critical illnesses and etc.

What is an investment-linked policy? How does it differ from others?

An investment-linked plan is a life insurance plan that combines investment and protection.

There are two types of investment-linked Policy (ILP); regular premium and single premium.

a) Regular Premium ILP

This is a regular premium paying ILP which provide financial protection together with investment element features in the product. ILP will provide flexibility, however the flexibility degree depends on the plan/riders being purchased. Policyholder may opt to change the investment funds offered by the insurer at any point of time. The policyholder can control the fund mix attached to the policy, change the protection amount, changed the premium direction at any point of premium payment made and withdrawal of fund at the prevailing unit price.

b) Single Premium ILP:

This is a single premium product with life insurance coverage. If the policy is still in force, the sum assured or the fund value; whichever is higher will be paid should there be any Death or Total and Permanent Disability (if coverage is not excluded). The policyholder may either partial withdraw or full withdrawal of the units and the fund value is based on the prevailing value of the fund.

Who will get the money when something happens to me, if death occurs?

We will pay to:

- competent nominee if there is no Trustee

- the trustee if there is a nomination

- the estate if there is no will or

- the assignee if we have been notified of an assignment

A non-Muslim policy owner may nominate a natural person(s) (i.e nominee(s)) to receive policy moneys payable upon his death under his policy. According to section 166 of the Insurance Act 1996, if the nominee is a spouse, child or parent (where there is no spouse or child living at the time of nomination), a trust shall be created automatically.

If the policy owner is a Muslim, the nominee shall act as an executor. He shall distribute the policy moneys in accordance with Islamic Law.

If there is a Dread Disease claim, such as disability or critical illness, we will pay upon total and permanent disability or diagnosis of a critical illness to the policy owner.

The claimant will have to notify the life insurance company and furnished documentary evidence to substantiate their claim.

What options do I have if I have financial difficulty and cannot pay premium?

a) Non forfeiture loan – If you have difficulty in paying the premium, you may keep the policy in force by non-forfeiture loan option if your policy has acquired cash value. The coverage will continue until the cash value is exhausted where the total indebtedness exceed the cash value available. The policy will then lapse.

b) You can convert the policy to a 'paid-up' policy where premium and the bonus declaration (if any) will be ceased but maintain the validity of the policy with the reduced sum assured.

What are the aspects to be focused on financial planning?

There are four aspects:

a) Insurance planning – this is to meet the financial security needs of yourself and your loved ones, should any mishap happen to you and/or your loved ones.

b) Investment planning – Plan and budget your income and expenses and let your money reap the returns according to your risk profile.

c) Retirement planning – plan for old age and ensure that you are able to continue to enjoy a comfortable lifestyle.

d) Tax planning - Ensure that appropriate taxes are being paid without having to make large sacrifices.

Why do I need to purchase Life Insurance for my Mortgage Loan?

Most banks required the mortgagor to take up mortgage insurance so that the family can still continue to live in the home even when they are no longer around. The sum assured of the mortgage insurance will utilize to settle the outstanding mortgage loan. Any amount in excess of the outstanding mortgage loan will be paid to the nominee/estate.

What is an assignment in Life Insurance?

An assignment is to transfer of the legal rights the insurance policy of personal property to another party. A life insurance policy can be assigned.

Assignment can be done either by Deed of Assignment signed by the assignor (policy owner) and the assignee (the party receiving the rights of the policy) via their own solicitor or by signing our company assignment form. Minimum stamp duty and registration fees are required.

What is Non Forfeiture Loan?

For those policy that had acquired cash value and if a premium is not paid within the 30 days of grace period, the policy will be kept in force by the non-forfeiture loan. Interest on such loan will be charged at a rate to be determined by the company. As cash value is utilized, it will reduce the overall benefit of the policy.

What does it mean by Lapse under Non-forfeiture Loan?

If the policy continue to be kept in force by non-forfeiture loan without any premiums paid, the cash value may exhausted when the outstanding of premium exceeds the cash value. The policy will eventually lapse.

What type of notices I should be expecting?

If the payment methods is other than direct debit or auto-debit arrangement and the mode of payment is other than monthly, our premium notice will be sent 1 month before the premium due date. If the payment is not remitted within 15 days from the due date, reminder will be sent. If payment is not paid within the 30 days' of grace, a lapse notice is sent if your policy has not acquired cash value. Otherwise, the Non forfeiture Loan notice would be sent.

For payment method through auto debit facility, if the deduction is unsuccessful, the company will send the unsuccessful deduction advice to the policyholder advising them to pay the premium to any of our branch nearest to them. If payment still not remitted, the policy may lapse (if the policy has not acquired cash value), lapse notice will be sent. Non-forfeiture loan statement will be sent if the policy has acquired cash value.

What particulars of my nominees do you require?

The information required is the name, date of birth, identification or birth certificate number, relationship, percentage of share and the address. This information will help us to speed up claim processing and with greater accuracy

Why do I need to appoint trustee?

If you are a non-muslim and had named either your spouse/child as nominees, or single with surviving parent as nominee, you are advised to name a Trustee. The role of the trustee(s) is to administer the policy money for the nominees.

How do I change my nominee/trustee?

Appointing New Nominee or Trustee - Notification for the Appointment of Nominee and Trustee (if the named nominee is either spouse/children or if single, naming the survival parents as nominee) form duly completed, signed and witness.

Change Nominee or Trustee (with existing Nominee or Trustee)

a) If the nominee is either spouse/children or is single naming surviving parents Any changes to the existing nominee will required the consent from the existing trustee (if any) or consent from existing nominee (if no trustee nominated) together with a fresh copy of nominee form duly completed, signed and witnessed.. If the purpose is to add nominee, all the existing nominee(s) is required to be stated in the fresh copy of nominee form.

b) If nominee relationship is not as pre stated in a. A fresh copy of the nominee form duly completed, signed and witness.

Premium Payment Methods

Go cashless!

Do away with carrying cash and join the cashless revolution for hassle free premium payments.

Log into our Customer Portal to sign up for auto debit via Debit/Credit card or simply complete an authorization form from our head office or any of our branches. It’s that easy!

Alternatively, you may also pay your policy premium online.

We have 5 cashless payment options for you to choose from.

1. Customer Portal

Pay your Tokio Marine Life insurance premiums via our Customer Portal platform.

Sign up as a user at our Customer Portal to pay online and manage your life insurance policy.

Steps to access Customer Portal online payment

a. Log on to Customer Portal

b. Login with your NRIC/ Passport Number and security password

c. Click on the ‘e-Payment’ tab in the menu bar

d. Select the policy you wish to make payment for

2. Auto Debit from Current/Savings Account

You can enrol to Auto Debit from your Current or Savings Account with Paynet Direct Debit.

Walk in to any of our nearest branches to arrange for Paynet Direct Debit with any of our participating banks.

Please check list of participating banks at here.

3. Credit Card Auto-Deduction

One of the most hassle-free option is to pay your premium via Auto Debit. You can arrange automatic deductions directly to your credit or debit card by following the steps below.

Credit Card Auto-Deduction via Customer Portal

a. Log on to Customer Portal

e. Login with your NRIC/ Passport number and security password

b. Click on the ‘Self Service’ tab in menu bar

c. Select ‘Credit/ Debit Card Payment (Auto Debit Instruction)’

d. Fill in all the mandatory fields

or Submit an Authorisation Form

a. Fill out the Credit/ Debit Card Debit Authorisation Form

b. Send the completed form to us via any of the following channels:

• Email: customercare@tokiomarinelife.com.my

• Fax: +603 2164 0988

• Walk in to any of our branches

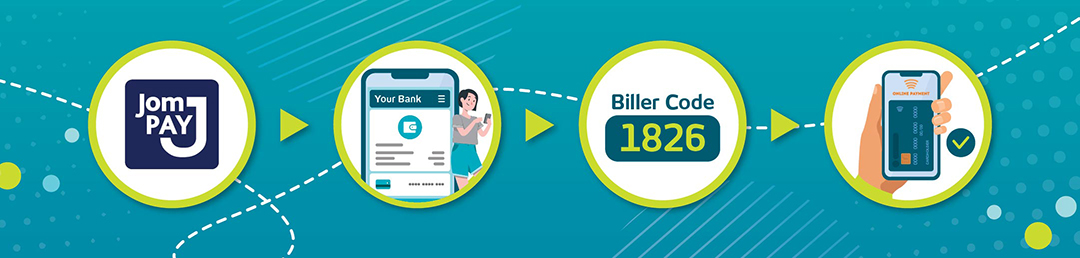

4. JomPAY

An easy payment solution for customers to pay policy premiums online via savings/ current account, or credit card.

4 quick steps to JomPAY (One policy per transaction)

a. Look for the JomPAY logo and the Biller Code number on your bills.

b. Log on to your preferred banking portal and select JomPAY.

c. Enter the Tokio Marine Life Insurance Biller Code (1826) followed by your policy number in Ref-1 and NRIC number in Ref-2.

d. Enter the premium amount to proceed with your payment.

5. Biro Angkasa

If you are an employee of a Government or Semi-Government body, or registered corporations, you can apply for your premium to be deducted from your monthly salary (for new proposal applications only). The application form for Biro Angkasa can be obtained from any of our Tokio Marine Life branches.

Disclaimer

By clicking on “Continue to external site” below, you will leave Tokio Marine Insurance Group’s website and you will be redirected to a third party website.

Choose your country or region

Visit HQ Pages

Visit Country Pages

Select your location and language

-

All

-

All

-

Asia Pacific

-

Australia

-

Americas

-

Europe

Singapore

Malaysia

Australia

You are currently on a site outside of your country Switch to external site?

Visit your local page. If you change your mind, you can use the dropdown at the top navigation to visit other Tokio Marine country pages.

Tokio Marine Life Insurance Malaysia Bhd. 199801001430 (457556-X)

You are currently on a site outside of your country. Switch to local site?

Visit your local page. If you change your mind, you can use the dropdown at the top navigation to visit other Tokio Marine country pages.